The ‘Midlife Money Crisis’ Nobody Talks About

You’re in your 40s or 50s. You’ve been working for decades. You’re doing everything “right.”

So why does it feel like you’re financially drowning?

If you’re nodding your head right now, you’re not alone. There’s a hidden struggle happening in midlife that nobody wants to talk about—a full-blown money crisis that’s affecting millions of people who thought they’d have it all figured out by now.

Let’s pull back the curtain on the midlife money crisis and, more importantly, talk about what you can actually do about it.

What Exactly Is a Midlife Money Crisis?

A midlife money crisis isn’t just about having less money than you’d like. It’s that suffocating feeling of being financially trapped when you’re supposed to be hitting your stride.

One in three people aged 50-55 rate their financial health as poor. That’s not a small percentage—that’s millions of people quietly panicking about their financial future while putting on a brave face for everyone around them.

This crisis manifests as constant stress about retirement, deep regret over past financial decisions, and an overwhelming sense that you’re running out of time to rectify things. You’re juggling rising costs, potential job insecurity, supporting family members who need help, and watching your retirement dreams slip further out of reach.

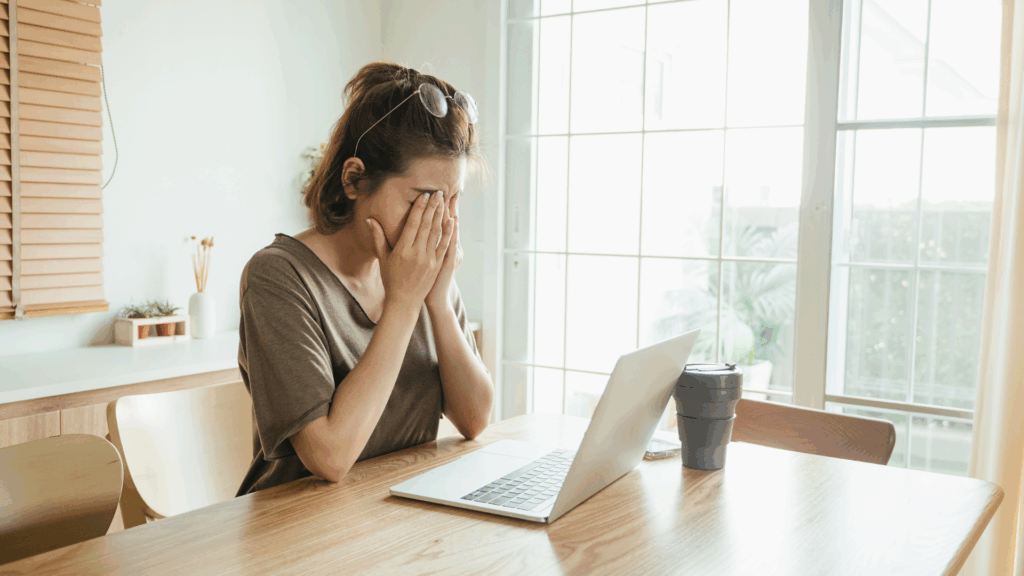

The emotional weight is crushing. Many people in this situation report feeling irritable, experiencing deep sadness, and sensing they’re boxed in by obligations with no way out.

The Hidden Emotional Toll Nobody Mentions

Here’s what the personal finance gurus don’t tell you: the money stress at midlife doesn’t just drain your bank account—it drains everything else too.

Financial struggles amplify stress, reduce happiness, and seriously harm both your physical and mental well-being. Money problems are directly linked to anxiety, sleep issues, and relationship stress. When you’re lying awake at 3 AM calculating whether you can afford to retire, that’s not just a money problem—it’s a health problem.

The regret hits differently at midlife. You look back at the opportunities you didn’t take, the savings you didn’t build, and the debt you didn’t avoid. That voice in your head keeps saying, “You should have known better” or “You should have done more.” It chips away at your confidence and makes it harder to believe things can get better.

When you’re also supporting adult children who can’t quite launch or aging parents who need financial help, the isolation gets even worse. You’re stuck in the middle, trying to hold everyone up while you’re sinking yourself.

Why We All Stay Silent About It

There’s a massive stigma around financial vulnerability at midlife. Society tells us we should “have it together by now.” Admitting you’re struggling financially in your 50s feels like admitting you failed at adulting.

We’re supposed to be the ones with wisdom and stability. We’re supposed to be role models for younger generations. So we stay quiet, smile through family dinners, and pretend everything’s fine while anxiety gnaws at us from the inside.

The pressure of the sandwich generation makes it worse. You’re expected to help your kids while also preparing to care for aging parents. How are you supposed to say “I can’t afford to help you” when everyone depends on you? The guilt is overwhelming.

Meanwhile, inflation keeps pushing prices higher, making it feel like you’re trying to run up an escalator that’s going down. Even if you’re doing everything the same way you always have, your money doesn’t stretch as far as it used to.

And honestly? Most people are just too exhausted to even look at their finances. When you’re working full-time, managing a household, and handling everyone else’s needs, sitting down to face your financial reality feels impossible. So we avoid it, which only makes the stress worse.

The Path Forward: Real Solutions That Actually Work

Here’s the truth: you’re not stuck forever. Yes, your situation might be challenging right now, but there are concrete steps you can take starting today that will make a real difference.

Get brutally honest about your spending and debt. The first step out of financial overwhelm is knowing exactly where you stand. Create a realistic monthly budget—not a punishment budget, but one that reflects your actual life. Track every dollar for one month. You might be surprised to see where your money is actually going.

Building an emergency fund should be your immediate priority. Even if you can only set aside $25 per week, start somewhere. Having 3-6 months of expenses saved reduces financial stress more than almost any other single action you can take. It’s the difference between a crisis and an inconvenience when life throws you a curveball.

Schedule a financial check-up. Think of it like a health screening, but for your money. Review your retirement accounts, list all your debts with their interest rates, assess your savings rate, and set achievable retirement goals based on your actual situation—not where you wish you were.

This might hurt at first. Looking at the numbers when you’re already stressed can feel overwhelming. But knowledge is power, and you can’t fix what you won’t face.

Deal with the emotional side. Money stress isn’t just logical—it’s deeply emotional. Naming your feelings about money can reduce shame and build confidence for change. Are you scared? Angry? Regretful? Embarrassed? Say it out loud or write it down.

Consider consulting a therapist who specializes in addressing financial stress. Yes, therapy costs money, but the mental health impact of unaddressed financial anxiety costs you more in the long run through poor decisions, health problems, and relationship damage.

Stop trying to do this alone. The DIY approach isn’t working if you’re reading this article. It’s time to get help. A financial planner can assess your situation objectively and create a realistic plan for your future. Many offer free initial consultations.

Community support groups for managing financial stress are available both online and in person. Talking with others who understand exactly what you’re going through breaks the isolation and gives you practical strategies that actually work in real life.

Prioritize your mental health alongside your finances. You can’t budget your way out of burnout. Regular self-care isn’t selfish—it’s necessary. Open conversations with loved ones about money stress reduce the burden. Stress-reducing activities, such as walking, journaling, or whatever helps you breathe more easily, make financial recovery possible instead of impossible.

When you’re constantly stressed, you make worse money decisions. You’re more likely to impulse spend, avoid dealing with problems, and give up on long-term goals. Taking care of your mental health is taking care of your financial health.

Small Steps Add Up to Big Changes

You don’t have to fix everything today. You probably can’t. What you can do is take one small action that moves you in the right direction.

Perhaps that involves opening a savings account and depositing $10. Maybe it’s making a list of all your debts. Possibly it’s calling your employer to see what retirement matching you’re leaving on the table. It may be as simple as admitting out loud to someone you trust that you’re struggling.

The midlife money crisis feels permanent when you’re in it, but it’s not. People recover from serious financial setbacks at midlife all the time. They rebuild their retirement savings, pay off crushing debt, and create financial stability. It takes longer than we’d like and requires making some tough choices, but it happens.

You’re Not Behind—You’re Just Starting From Here

Stop beating yourself up about where you “should” be financially. Regret doesn’t pay the bills or build your retirement account. What matters now is what you do from this point forward.

Your 40s and 50s aren’t too late to change your financial picture. You likely have 15-25 years of work left. That’s enough time to make significant progress if you start taking action now, rather than waiting until retirement is six months away.

The financial stress you’re feeling is real and serious. But you have more control than you think. You can’t control inflation, the economy, or past mistakes. You can control what you do today.

Take one step. Then take another. Ask for help when you need it. Be honest about your situation. Give yourself grace while also holding yourself accountable.

The midlife money crisis nobody talks about? You’re talking about it now. And that’s the first step toward getting through it.

What’s Your Next Move?

If you’re dealing with midlife money stress, what’s the one thing you’re going to do this week to start taking control? Opening that savings account? Scheduling a meeting with a financial advisor? Finally tracking your spending?

You don’t have to share publicly if you’re not comfortable, but commit to yourself. Write it down. Put it on your calendar. Then do it.

Your future self will thank you for taking the first step today.